MBW Explains is a series of analytical features in which we explore the context behind major music industry talking points – and suggest what might happen next. Only MBW+ subscribers have unlimited access to these articles.

One of the biggest music business stories of the year has been missing something: official confirmation.

And did SMG then splash a further USD $400 million on Pink Floyd’s recorded music catalog, plus ‘name, image, and likeness’ rights?

Enough industry sources and credible media reports have combined to quasi-confirm that yes, it did.

Earlier this month, speaking to Bloomberg in Los Angeles, SMG boss Stringer publicly verified for the first time that Sony has bought both these historic catalogs (even if he didn’t confirm the price).

Stringer further confirmed that Sony recently acquired a stake in Michael Jackson’s catalog, a deal which is thought to encompass 50% of the King of Pop’s music rights portfolio.

If you believe industry whisperers (MBW included), Sony — backed by cash from Apollo — has cumulatively spent over $2 billion combined on MJ, Queen, and Pink Floyd.

So why did Stringer and Sony lay down such vast sums on these vintage catalogs? And, Jackson aside, why has Sony bet so big on ‘classic rock’ in an age when it’s far from the dominant genre on streaming services?

Here are three good reasons…

1) ‘eventized’ potential

At Bloomberg’s event this month, Rob Stringer confirmed that Sony acquired “name, image, and likeness” rights to two of the three acts in question. We know Pink Floyd is one; he didn’t confirm the other.

Stringer suggested that acquiring these ‘NIL’ rights would enable Sony to creatively and financially participate in the “experiential potential” and “event potential” they offer.

Images of ABBA Voyage immediately spring to mind: the idea of replicating the imagery and sound of a legendary act, in multiple venues across the world, via cutting-edge technology.

Could ABBA Voyage-esque productions, owned by ‘name & likeness’ domain-holders, eventually become the new ‘tribute band’?

If so, no wonder Stringer’s seeing dollar signs.

The Australian Pink Floyd (TAPF), to pick one example, has regularly appeared in Pollstar’s quarterly Top 100highest-grossing concert lists in recent years.

Credit: Sony Music Group

“It’s like an act touring times-five – that’s quite lucrative!”

Rob Stringer on Sony’s stake in MJ: The Musical, and the fact it can play in multiple cities on the same night

The continuing popularity of the Aussies’ copycat Pink Floyd ‘experience’ is no great shock: people sometimes forget that the real Pink Floyd secured the biggest-grossing global live show of the whole of the 1980s with the A Momentary Lapse Of Reason tour.

(Yes, it grossed even more than Michael Jackson’s legendary Bad tour that decade – though Floyd played 197 shows vs. MJ’s 123.)

The idea of a Sony-owned or co-owned “experiential” production, playing in multiple locations each evening, is clearly one Stringer likes very much.

“[Sony] has a share of MJ: The Musical, a percentage with the Michael Jackson estate, as does our picture company,” Stringer confirmed at the Bloomberg event.

Stringer said versions of this musical would be playing in five cities worldwide over the next year (potentially at the same time).

That, he said “is like an act touring times-five – that’s quite lucrative!”

2) Classic Rock isn’t dead… it’s streaming like wild

‘Name, Image, and Likeness’, then – and where ownership of it might lead in the live space – is a crucial part of why Sony spent what it did on these catalogs.

So too is physical music and merch sales – another beneficiary of ‘NIL’.

But there’s a more modern reason why Stringer and SMG splashed the cash: streaming.

At this point, you might think, “Streaming’s all very well for Michael Jackson, but vintage rock like Pink Floyd isn’t exactly down with the kids.”

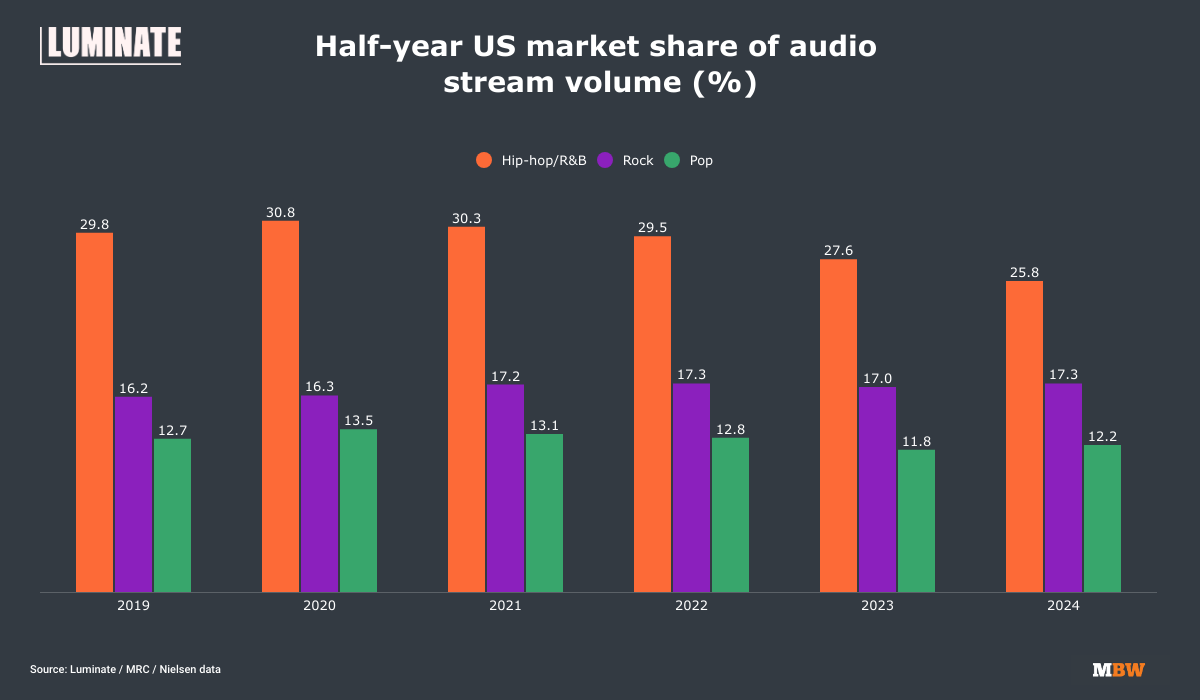

On the surface, you’d be right: Below you can scan a chart based onLuminate‘s recent mid-year market report (and other comparable historical reports showing half-year data for the US).

It shows the popularity of the three biggest genres in the US – ‘Rock’, ‘Pop’, and ‘R&B/Hip-hop’ (as categorized by Luminate) – in the Jan-Jun period over the past few years.

As you can see, ‘Rock’ has slightly grown share during this timeline, but: (a) It hasn’t spectacularly gained market share, up 110 basis points since 2019; and (b) that’s despite a significant decline (minus 500 basis points) in market share for ‘R&B/Hip-hop’ since 2020.

(Latin Music has been the big market share gainer since H1 2019, growing from a 4.2% mid-year share that year to 8.3% in H1 2024.)

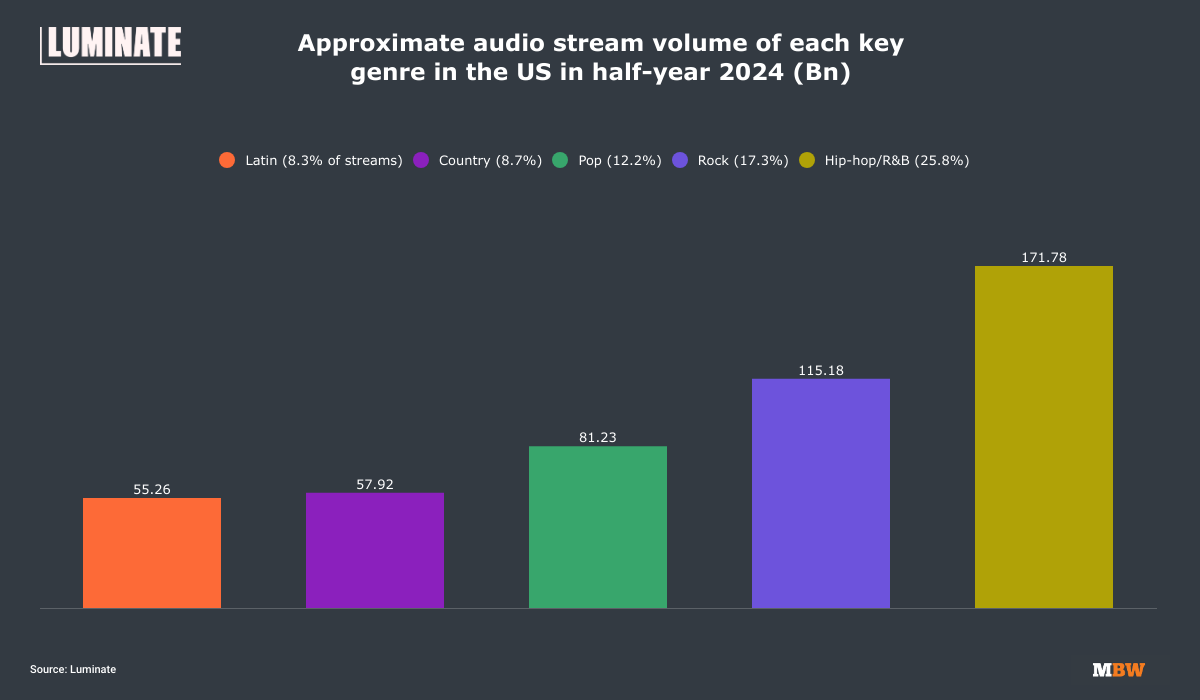

By taking the above stats and applying them to the total audio streams in the US market in H1 2024 (all 665.8 billion of them), we can estimate the total stream volumes for each genre in the period.

This is arguably a better illustration of the gulf between the most popular genres in the States.

Again, ‘Rock’ doesn’t do badly in this picture, but as you’d expect, it’s dwarfed by ‘R&B/Hip-hop‘.

But now look.

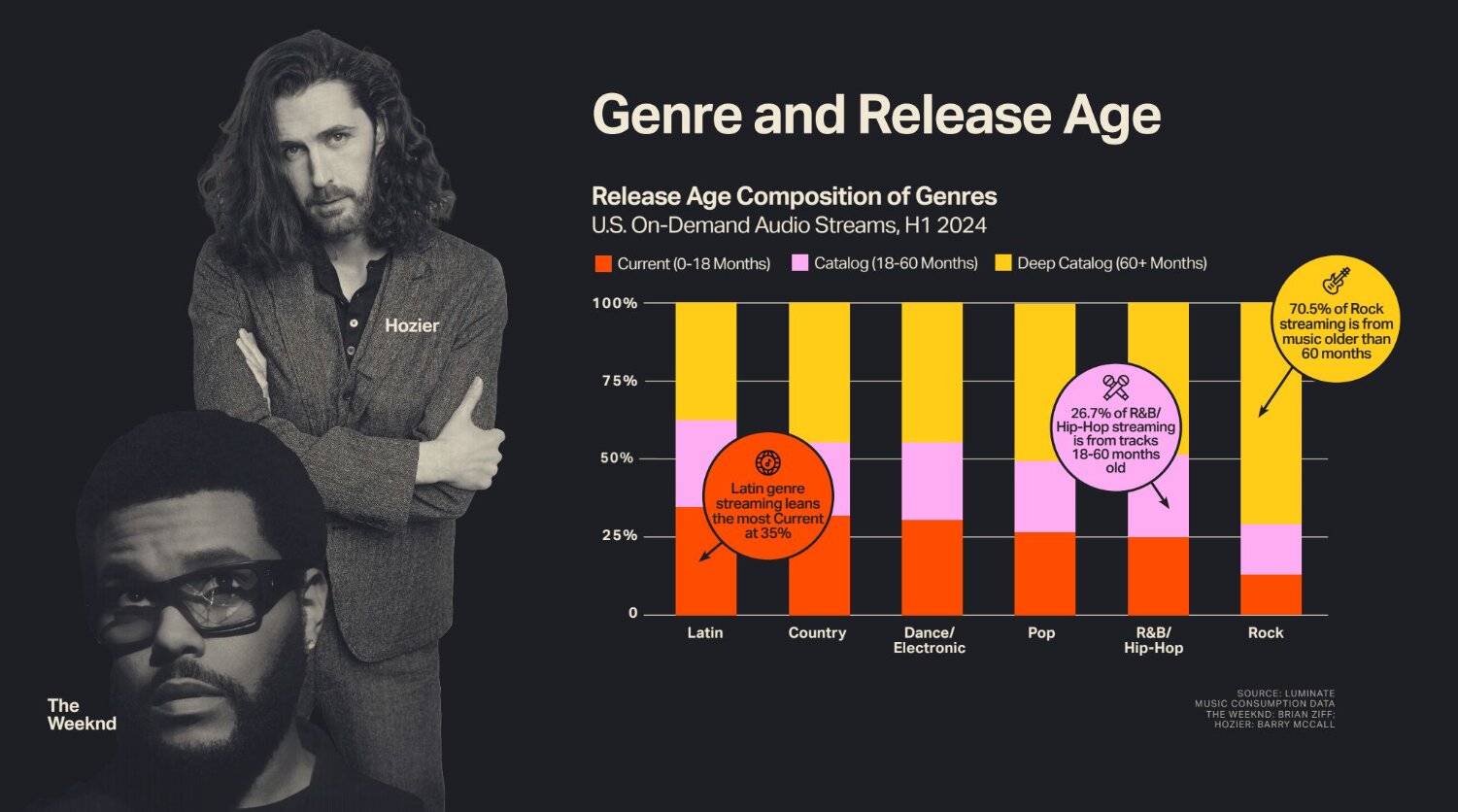

Luminate’s mid-year 2024 report includes the slide below, which gives an approximate impression of the percentage of total streams within each genre that are from tracks that are less than five years old vs. tracks that are more than five years old.

This tells us, in one snapshot, that the popularity of ‘R&B/Hip-hop’ appears to be far more reliant on new releases than ‘Rock’.

Over a quarter (26.7%) of R&B/Hip-hop tracks streamed in H1 2024 were less than 60 months old, while nearly three-quarters of ‘Rock’ tracks (70.5%) were more than 60 months old.

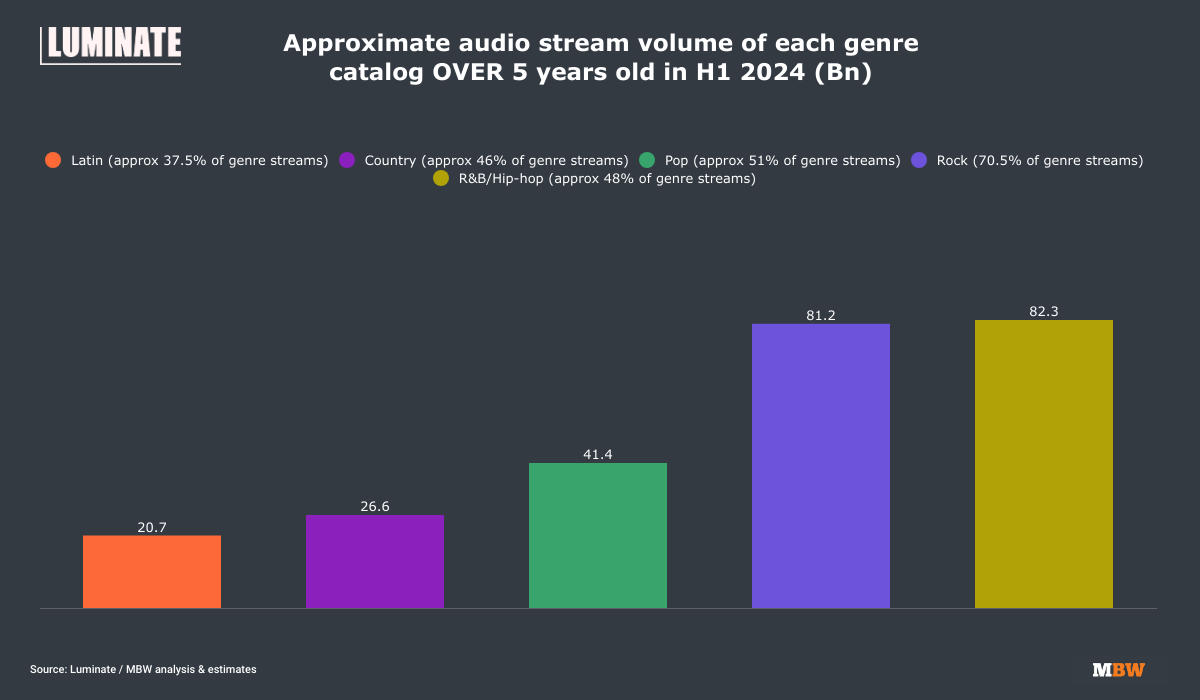

Now, let’s take the approximate figures above and apply them to actual H1 2024 US stream volumes divided by genre.

This gives us new insight into how each genre fares in real terms if you only count streams of music older than five years/60 months (‘Deep Catalog’).

(Warning: some of this is guesswork based on my own eyes. Luminate confirms numbers for three genres in the above chart, but for other genres it offers an indicative colored chart. For example, looking at the above, it appears that 48% of ‘R&B/Hip-hop’ streams – the yellow bar – were of ‘Deep Catalog’ in the period, judging by the values on the Y axis.)

Conclusion: when you only consider music older than five years, in the first half of 2024, ‘Rock’ near-or-less kept pace with ‘R&B/Hip-hop’.

Pink Floyd is 209th, with 10.07 billion plays – ahead of the likes of Mariah Carey, The Rolling Stones, Enrique Iglesias, and ABBA.

3) When they zig, you zag… especially if currency’s on your side

There are plenty of other potential factors worth mentioning for Sony’s big-spending on catalog music titans in recent months, including interest and exchange rates in Japan.

As interest rates have ballooned in the ‘West’ over the past few years, restricting the willingness of blockbuster spending on music catalogs, interest rates in Japan – set by the Bank Of Japan (BoJ) have typically been negative in the same period, at around -0.10%.

More recently, Japan’s interest rates have climbed to +0.25%, the highest since 2008, but still considerably lower than the US/UK/EU (see below).

Japan’s interest rates as per the Bank Of Japan over the past few years (source: TradingEconomics)

Meanwhile, Japan’s Yen has weakened significantly against GBP and USD in recent years.

Example: as recently as February 2021, one US Dollar would have cost you 0.0092 Yen; today, that same dollar costs 0.0065 Yen.

Putting that in simpler terms: if you wanted to spend USD $400 million on Pink Floyd’s catalog today, and you were converting the cash to pay for it into USD from Yen, it would currently cost you around a third less (in Yen terms) than it did three years ago.

Sony would, therefore, be able to take advantage of currency trends by acquiring US/UK-based catalogs with its Japan-based treasury. (And it’s a seriously large treasury: Sony Corpended its latest FY in March with 1.907 trillion Yen in cash and cash equivalents – currently worth around USD $12.5 billion.)

The Japanese corporation would also potentially be able to borrow debt locally at far cheaper rates than US, EU, or UK companies if required.

(Then again, Sony Music Group might not even have needed all that much money from its parent: don’t forget that Apollo led a $700 million “capital solution” for SMG earlier this year, money that would have been put to good use in the Pink Floyd deal, and likely the Queen deal too.)

Bottom line: Sony Music Group’s access to capital isn’t in question.

This might partly help explain why, when its rivals have appeared to ‘zig’ on blockbuster single-artist catalog deals – slowing down the big-spending we saw at the height of the market – Sony has ‘zagged’, spending more than ever.

Universal Music Group, for example, has yet to publicly announce any large-scale catalog acquisitions via Chord Music — the $1.85-billion-valued vehicle UMG minority-owns (and Dundee Partners majority-owns), as announced in February.

We’ve also seen overall value slowdowns in catalog pipeline deals in the past 12 months at companies including Reservoir and BMG, while consolidation has hit music’s catalog M&A sector elsewhere: witness the sale of music catalogs from Round Hill, Opus, and Vine Alternative Investments to rival music companies.

(It’s only right to point out that, amid this slowdown, the likes of Concord and Litmus have still pulled off multiple nine-figure acquisitions of artist catalogs.)

That figure ($2.2 billion) is approximately, according to reports, the same amount Sony has spent on just three catalog deals: Queen, Pink Floyd, and 50% of Michael Jackson.

Speaking to Bloomberg this month, Rob Stringersuggestedthat Pink Floyd’s recorded music catalog was essentially priceless, and that buying it was tantamount to an art collector buying a Picasso.

In some ways, that analogy doesn’t quite fit: someone acquiring a Picasso is unlikely to earn hundreds of millions from it in royalties and T-shirts over the course of its copyright-able lifetime.

Yet in another sense, Stringer’s analogy perfectly reflected his company’s philosophy in these deals.

After all, no serious art investor buys a priceless Picasso without feeling confident that in ten years, or fifty years, it will be worth significantly more than it is today.Music Business Worldwide