The United States is squandering its best opportunity to compete in the global battery race. China jumped to a commanding lead in the last decade, controlling the supply chain for lithium-ion batteries, which power everything from cell phones, to military drones, to electric vehicles (EVs). By passing ambitious legislation under U.S. President Joe Biden, Washington has begun investing heavily in its domestic battery industry.

But even significant funding won’t get the job done if it isn’t directed at the right target: securing U.S. supremacy in next-generation technology, solid-state batteries. U.S. companies and research institutions are on the cusp of commercializing next-generation batteries that far surpass the performance of today’s lithium-ion batteries in safety, longevity, and energy density. And with scaled-up production, these batteries would eliminate dependence on Chinese-produced graphite.

The United States is squandering its best opportunity to compete in the global battery race. China jumped to a commanding lead in the last decade, controlling the supply chain for lithium-ion batteries, which power everything from cell phones, to military drones, to electric vehicles (EVs). By passing ambitious legislation under U.S. President Joe Biden, Washington has begun investing heavily in its domestic battery industry.

But even significant funding won’t get the job done if it isn’t directed at the right target: securing U.S. supremacy in next-generation technology, solid-state batteries. U.S. companies and research institutions are on the cusp of commercializing next-generation batteries that far surpass the performance of today’s lithium-ion batteries in safety, longevity, and energy density. And with scaled-up production, these batteries would eliminate dependence on Chinese-produced graphite.

Yet a majority of the U.S. funding spree has so far supported current-generation technology, lithium-ion batteries—an expensive and likely futile attempt to wrest market share from China. Of the $30 billion that the U.S. government has committed to battery investments in the last two years through grants, loan guarantees, and tax incentives, more than 90 percent supports lithium-ion batteries. To be sure, it is prudent for the United States to secure a limited supply of lithium-ion batteries, produced either domestically or by trusted partners abroad, to hedge against the risk of China cutting off exports of batteries or their components.

But the United States cannot build a globally competitive battery industry that does not require unending subsidies if it relies only on today’s technology.

It’s time for a decisive shift in Washington’s strategy. Although policymakers have already spent tens of billions of dollars largely on today’s technology, there are still major opportunities to redirect future funding. The United States can leapfrog China’s global lead through a three-pronged approach: refocusing incentives to boost the production of advanced batteries, targeting public procurement at next-generation technologies, and expanding research and development funding.

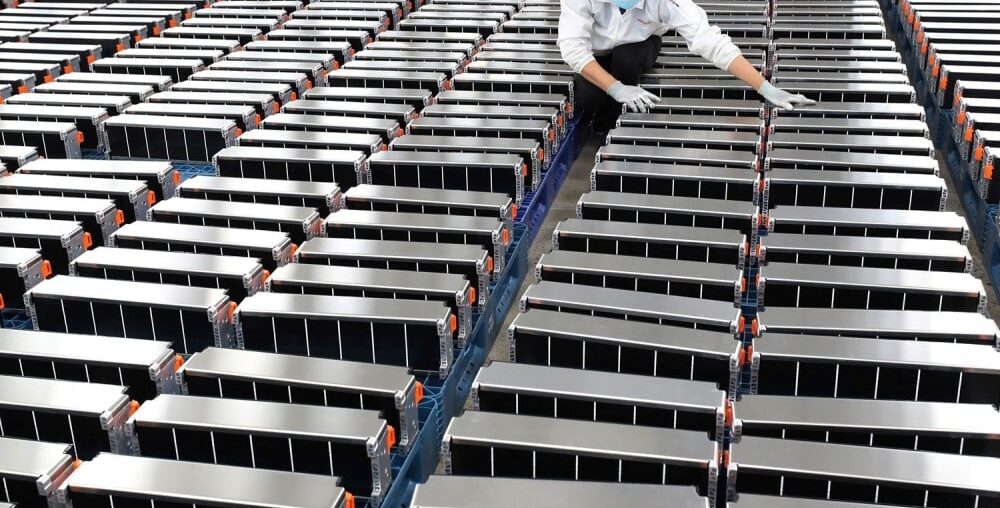

China has already won the race to mass produce lithium-ion batteries. Across the entire value chain for this technology—mining, material processing, and cell and pack manufacturing—it controls more than 80 percent of the global market. Japan and South Korea continue to play important roles in niche parts of the supply chain, but the United States and Europe are far behind in terms of competitiveness. Today, the United States relies heavily on battery imports from Asia; China alone supplied 72 percent of the U.S. market last year.

China’s daunting lead is the result of more than two decades of investment, dating back to its 2001 Five-Year Plan, which made batteries and electric vehicles a strategic economic priority. Since 2009, Beijing has provided $230 billion in government support to domestic EV and battery manufacturers and built a global network of battery supply chain investments, from critical mineral mines in Africa and South America to processing and manufacturing units back home.

The United States will thus struggle to play catch-up with China and build a cost-competitive lithium-ion battery industry. Even if it could, the rewards wouldn’t be worthwhile. China has a dire oversupply problem; its lithium-ion battery production capacity exceeds global demand by 400 percent. U.S. batteries are at least 20 percent more expensive to manufacture than Chinese batteries due to the tremendous economies of scale and integrated supply chains in China. Despite the recent boom in U.S. battery investment, it’s hard to see that gap closing, especially after Beijing’s plan to double down on manufacturing and exporting clean-energy products.

Yet the stakes are too high for the United States to cede the field in battery technology. The race to commercialize the next generation of battery technology is far from over—and the prize is massive. Next-generation batteries unlock dramatic performance gains by replacing key components of today’s batteries, such as graphite anodes and liquid electrolytes, with pure lithium metal anodes and a solid-state architecture. These solid-state batteries have been hailed as the “holy grail” of battery technology, and companies could sell the premium batteries at higher profits than producers of today’s technology.

With greater energy storage and faster charging and discharging capabilities, these batteries could enable long-distance drones and EVs, as well as more powerful consumer electronics. They could be more durable while avoiding the safety risks of today’s flammable lithium batteries, which have caused deadly accidents this year by exploding in buildings and ocean tankers. Most importantly, these batteries would eliminate U.S. dependence on graphite—a critical material over which China has a chokehold on production and has used export controls to hamper Western competitors.

China is deeply concerned that this new technology could upend its current dominance in the global battery market. While Chinese companies are in a leading position to wring efficiency gains out of lithium-ion batteries, U.S. companies and universities have been investing in solid-state technology for more than a decade. The largest U.S. solid-state battery firm, QuantumScape, is scaling up production of next-generation batteries with the Volkswagen Group for use in high-end electric vehicles.

Yet with a market capitalization of almost $3 billion, the largest U.S. firm is still a minnow compared with China’s battery champions CATL (valued at approximately $144 billion) and BYD ($109 billion), South Korea’s Samsung ($290 billion), and Japan’s Toyota ($227 billion), all of which are also racing to commercialize solid-state batteries.

Governments are not passive observers of this race. China, in particular, is investing heavily in solid-state battery development, having assembled a billion-dollar fund to help its domestic champions produce these batteries first. To win, the United States needs to step up its game.

First, Washington needs to prioritize incentives to boost the production of advanced batteries. Current and future policymakers will have wide discretion to support this. For example, the 2021 Bipartisan Infrastructure Law allocated funding for the broad category of “advanced batteries,” under which the U.S. Energy Department can easily fund both next-generation and current-generation technologies.

The next opportunity to support leapfrog technologies will come when the Energy Department awards $6 billion in tax credit allocations under the 2022 Inflation Reduction Act (IRA). The Biden administration should use this to sharply increase its allocation of funding for solid-state batteries. Moving forward, the U.S. Congress should build on the IRA by focusing new tax incentives on manufacturing for next-generation batteries because producers of existing technologies will almost certainly monopolize today’s incentives, such as the IRA’s 45X tax credits for battery manufacturing.

To some extent, producing lithium-ion batteries can help the United States leapfrog to next-generation technologies by ensuring a solid base of firms and workers with experience making batteries. Plus, many of the critical minerals used in lithium-ion batteries—such as lithium, nickel, and cobalt—are also critical for solid-state batteries. Still, the current split between funding existing and next-generation technologies is imbalanced. A surge in funding for solid-state technology could address a critical need: helping U.S. companies bring these batteries out of the laboratory and into pilot-scale—and then commercial-scale—manufacturing.

Second, the U.S. government needs to target public procurement at next-generation technologies. U.S. companies developing solid-state batteries need more than funding to commercialize their technologies—they also need customers to buy their batteries. U.S. government procurement can provide an ideal initial market. The military should dedicate a small niche of its procurement for drones, military vehicles, and field equipment for solid-state batteries made in the United States.

Other government agencies, such as the U.S. Postal Service, should devote portions of their procurement of EVs to those that use solid-state batteries produced in the United States, too. These procurements can be more expensive than simply purchasing market-rate equipment and vehicles, so Congress should explicitly authorize such procurements to enable the government to prioritize innovative, U.S.-made products. Crucially, this targeted procurement should not last forever. As the U.S. next-generation battery industry scales up, funding and procurement should ramp down, so that U.S. firms can compete with global ones.

Finally, the United States should continue to press its innovation advantage. U.S. universities, research institutions, and laboratories will need more funding to redouble their efforts and compete with their Chinese counterparts. China’s aggressive innovation investments are already paying dividends; Chinese research institutions now account for nearly two-thirds of highly cited battery technical papers, compared with only 10 percent from U.S. institutions.

Ultimately, the United States should play to its strengths; innovation has always been a hallmark of U.S. competitiveness. But breaking the China cycle—in which technologies developed in the West are perfected, scaled, commoditized, and mass-produced in China—will require a holistic, competitive strategy from the United States. Washington has already lost the race for current-generation batteries, but it can’t afford to squander the opportunity to win the next one.