In the past two months, a raft of reports relating to Vanuatu’s economy have been released: the national government’s Half Year Economic and Fiscal Update, the International Monetary Fund’s Article IV report, the Asian Development Bank’s Pacific Economic Monitor plus government tourism and trade statistics.

When these are read together it is hard to avoid the conclusion that there is an emerging economic emergency in Vanuatu.

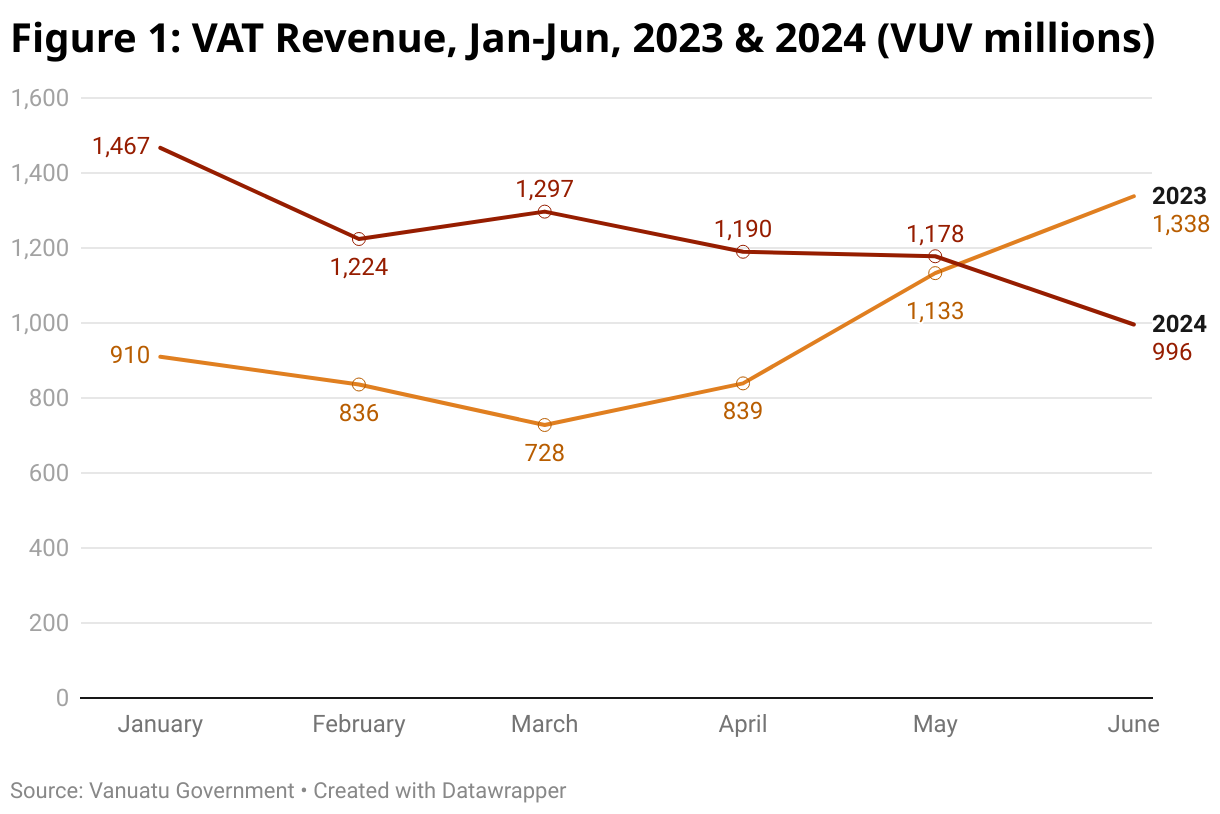

The simplest metric to measure economic activity is the quantity of Value Added Tax (VAT). This started the year off in record fashion, but the liquidation of Air Vanuatu had a clear and crushing impact. VAT returns in June (VUV996 million) were 25% lower than the year before (VUV1,388 million).

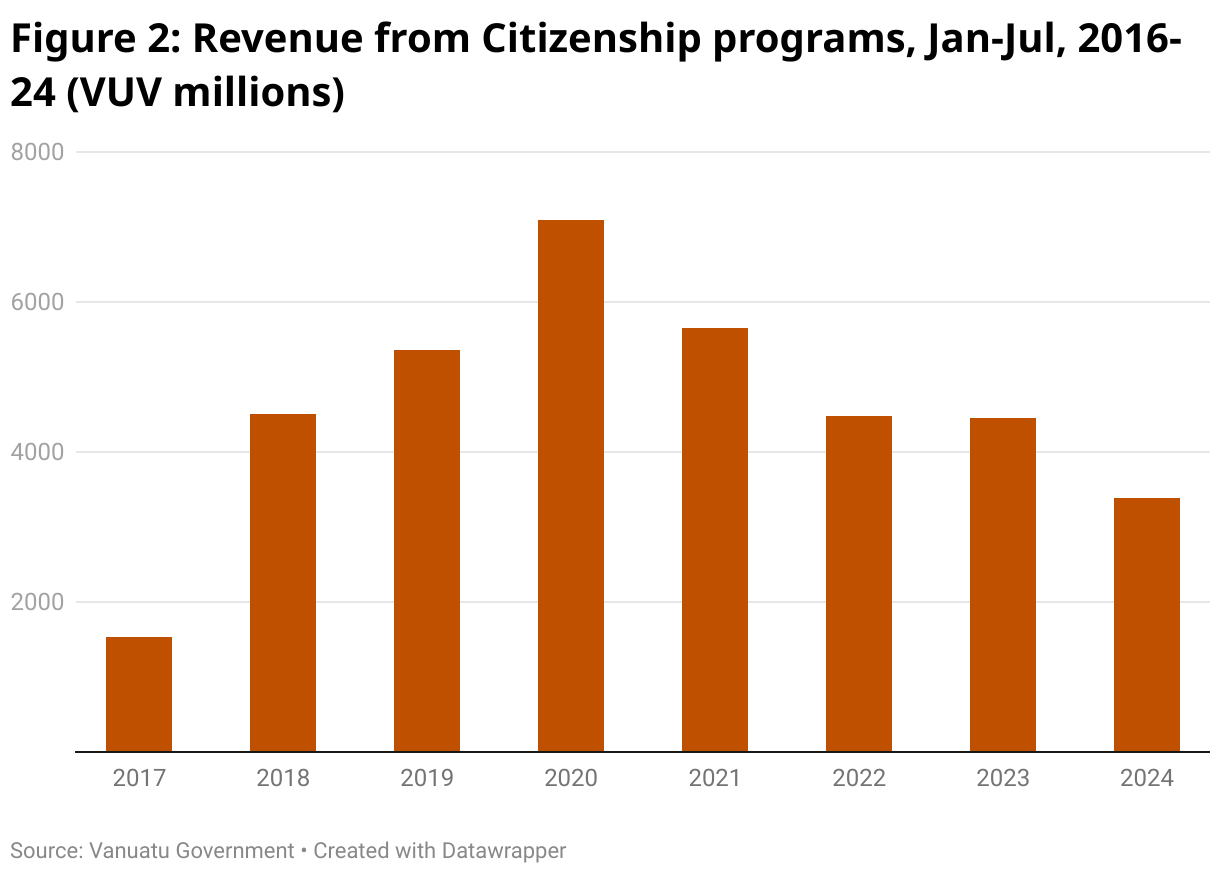

This is part of a broader crisis in government revenue, which was 23% below target from January until June, with no single revenue source meeting its target. Citizenship program revenue is the biggest concern, with revenue down 24% on 2023 and 50% on the 2020 peak. (The Citizenship By Investment Program, formally known as the Vanuatu Development Support Program, is a program which allows foreign citizens to purchase passports and gain visa-free travel to more than 80 countries.)

The World Bank estimates that the economy is 3% smaller than in 2019, and that real GDP per capita (approximately income per person) is US$2,517 (VUV 205,602). This is 11% lower than in 2019, and 8% lower than in 2000. There is no country at this income level which provides core government services to an acceptable quality.

The national government is forecasting annual growth of 3.8% from 2025 to 2028, and the IMF forecasts just 2% annual growth until 2044. With the population growing at roughly 2% yearly, this would mean limited improvements in the quality of life.

This would be concerning normally, but with the climate emergency looming, it is critical. The economic costs of the crisis will be huge, and the single best way to adapt to it is to get richer. Constant technological and geopolitical upheavals make it all the more important for Vanuatu to become more resilient.

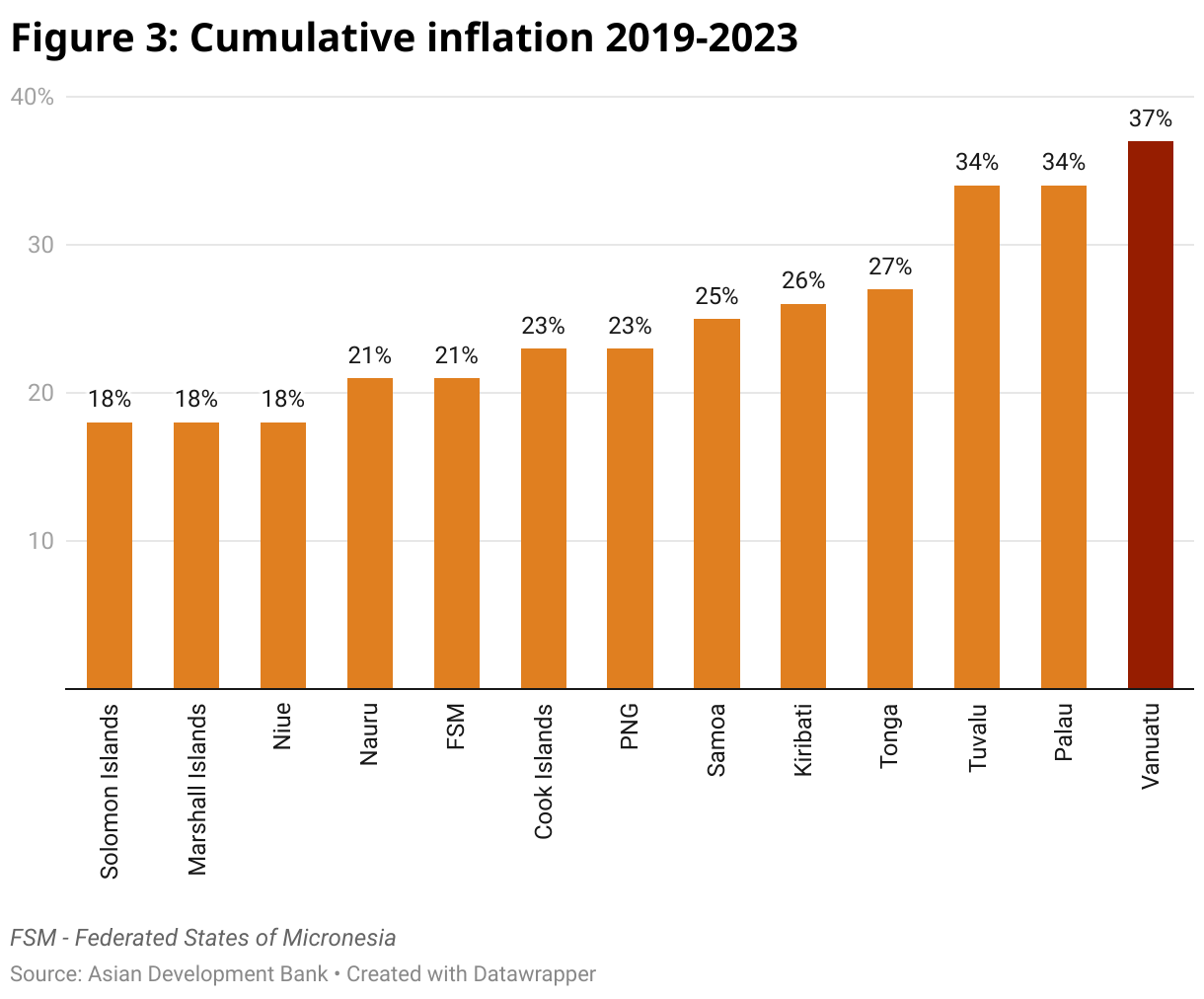

In the face of these challenges, Vanuatu should be aiming for a growth rate of at least 7% until at least 2050. To achieve this, there must be a drastic expansion in productive capacity – the amount of goods and services an economy can produce. Limited productive capacity is one of the reasons Vanuatu has had the highest inflation in the Pacific since 2019.

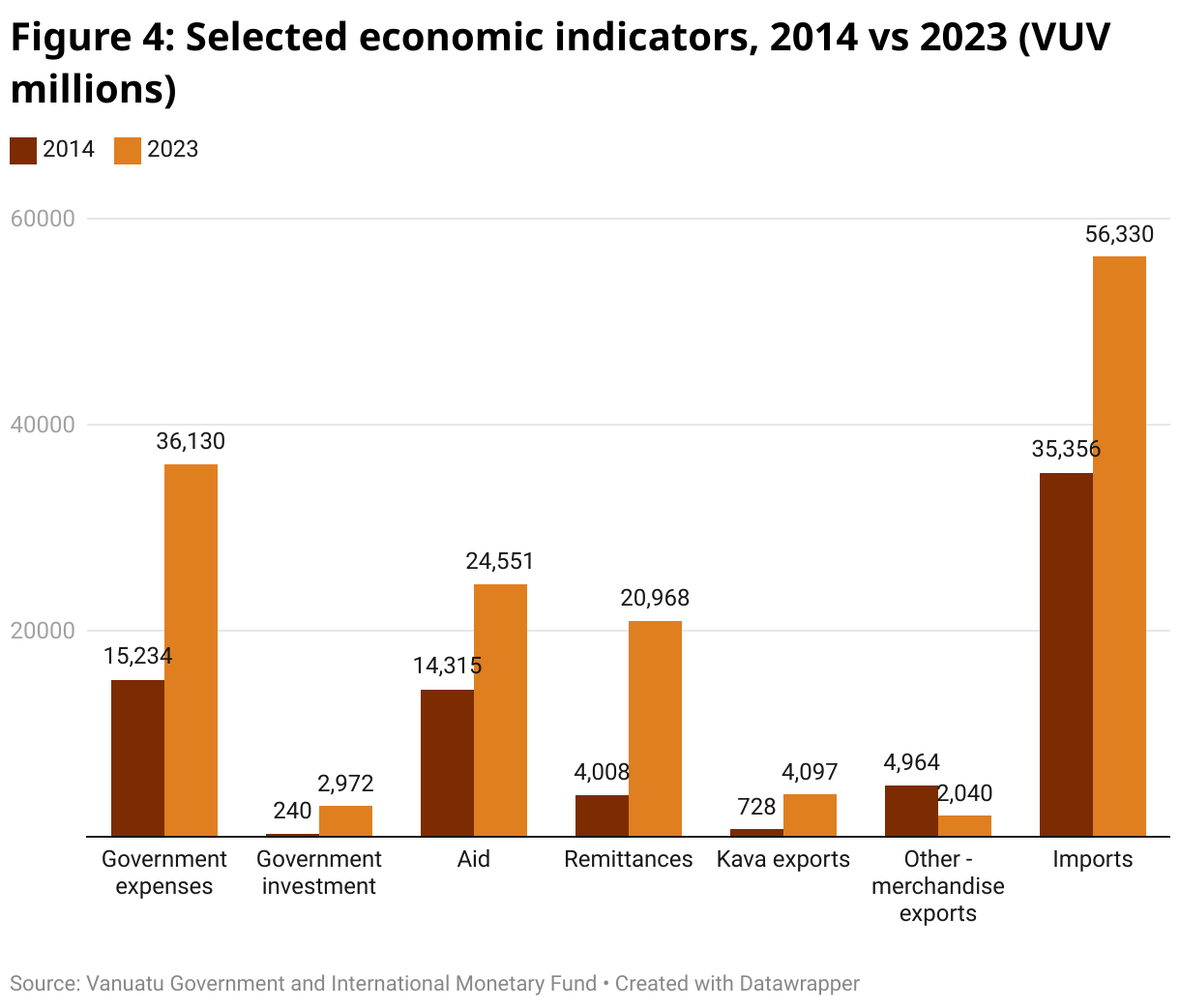

Far too much of the growth of the past decade has failed to boost productive capacity. This is particularly true of growth driven by citizenship sales, aid and remittances. Of course, these all have major positives, but they also all involve large amounts of money flowing into the economy that has not been earned within Vanuatu, much of which flows straight out again through imports.

To boost productive capacity, Vanuatu needs huge amounts of good investment — this is what builds genuine wealth and resilience over the long-term.

The government is currently spending but not investing. Expenses (day-to-day spending) hit a record high in the first half of 2024 (VUV19.7 billion), but investment remains low and slow. Just 4.6% (VUV790 million) of the capital budget for the year had been spent by June.

Forecasts for government expenses are steady, while government investment forecasts for 2025-2028 have been downgraded from VUV22 billion to VUV15 billion.

The IMF is calling for fiscal consolidation (cutting spending) in response to the revenue issues. Somehow, they have not learnt from their own long and disastrous history what awful policy this is. Following this advice has already caused major issues in the past six months in Kenya, Ghana, Sri Lanka and Bangladesh, and no-one can seriously argue that the government is spending enough to deliver the most basic services.

Over the long run, the only way that higher spending can be sustainable is if the economy is far larger. Most of this growth will have to come from the private sector. Businesses have endured a brutal decade of natural disasters, COVID, political instability and consistent air connectivity issues. As a result, private sector confidence and trust is low.

Foreign direct investment was just 0.9% of GDP in 2023, well below the historical average. There is limited data on domestic investment, but there is definitely not enough.

Merchandise exports were just 8% higher in 2023 than in 2014, far below both inflation and population growth. Food inflation has been 60% over this period, with many increasingly struggling to afford healthy food. Visitor arrivals by air were 29% lower in 2023 than in 2014 and they have fallen a further 28% this year.

The business environment remains extremely challenging, with access to skills the biggest issue. A country’s most important resource is its people but heartbreakingly the current generation of children is categorically not being given the tools needed. Three out of ten children are stunted, while eight out of ten failed to meet the minimum standard for Year 4 Literacy in the most recent Pacific-wide assessment.

But in the face of all of these challenges, there remains cause for immense optimism. The full case for this is at least a whole article in itself, but three key points are briefly made below.

First, Vanuatu is a wonderful, peaceful and friendly country, and many of its foundations are extremely strong; often more so than in richer countries.

Second, emerging technologies mean that the economic story could be completely transformed in a very short timeframe.

Third, there has been undoubtedly been rapid progress in many areas, and we must not forgot that progress.

It’s also the case that a number of good initiatives have been announced recently, such as the increasing digitalization of government and the townships project. But, of course, there is much more that must be done.

One idea is to set up an Economic and Investment Committee, chaired by the Prime Minister, with a single goal of achieving 7% economic growth. The Economic and Investment Forum in March this year generated 80 ideas for improving the business environment. Such a committee could go through these ideas and rapidly implement the best.

However, the full impact of many reforms would not be felt for years, and would not solve the immediate revenue issues.

I would therefore suggest that VAT is increased to 20%. The emerging economic emergency means that drastic action is needed, and VAT is the only lever that can provide the required revenue in the timeframe required.

Of course, this would be highly controversial and painful, particularly for those struggling the most. For the policy to work, two things must happen.

First, there must be an accompanying major improvement in how the government spends money. Inefficient and wasteful spending must be replaced by quality investment for the long-term future of Vanuatu. The devastating Off-Budget Entities Report is a clear indicator of the need for urgent reform.

Second, part of the revenue raised should be used to reform the business environment. To this end, I would also suggest that nearly every single fee and charge is completely abolished, and that a 10% VAT rate is applied to key sectors (such as shipping, Vanuatu-made goods and construction). This can be done almost immediately, and it would both make a major difference to the ease of doing business and send a strong signal that the government is serious about reform and growth.